How To Finance Mudra Loan ? – MUDRA Loan stands for Micro Units Development & Refinance Agency Limited is an institution being set up by Government of India for development and refinancing activities relating to micro units.

The purpose of MUDRA Loan is to provide funding to the non corporate , Non Agricultural small business sector. MUDRA has created the categories named ‘Shishu’, ‘Kishor’ and ‘Tarun‘ to signify the stage of growth / development and funding needs of the beneficiary micro unit and also provide a reference point for the next phase of growth to look forward to :

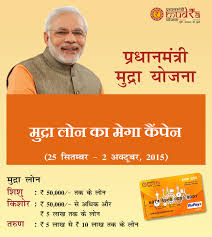

Shishu : covering loans upto 50,000/-

Kishor : covering loans above 50,000/- and upto 5 lakh

Tarun : covering loans above 5 lakh and upto 10 lakh

This is made mandatory to finance at least 60% of the credit flows to Shishu Category Units and the balance to Kishor and Tarun Categories.MUDRA have also defined the roll out stage designed to meet requirements of different sectors / business activities as well as business segments. Briefly :-

Sector and activity specific schemes

Micro Credit Scheme (MCS) for businesses

Refinance Scheme for Regional Rural Banks (RRBs) / Scheduled Co-operative Banks

Mahila Uddyami Scheme

Business Loan for Traders & Shopkeepers

Missing Middle Credit Scheme

Equipment Finance for Micro Units

There are much confusion among the bankers or lending institution or Loan Officers in financing the MUDRA loan. Sometimes they could not differentiate among the various categories of loan to be finances. This is the elaborated list which can be financed under MUDRA yojana.

The Various categories which may be financed under MUDRA Yojana by different banks :

1. Land Transport Sector : This should be financed exclusively for purchase of transport vehicles for goods and personal transport such as auto rickshaw, small goods transport vehicle, 3 wheelers, e-rickshaw, passenger cars, taxis, etc. To be remember these transport categories must support the existing running/proposed units.

2. Community, Social & Personal Services : All activities such as saloons, beauty parlors, gymnasium, boutiques, tailoring shops, dry cleaning, cycle and motorcycle repair shop, DTP and Photocopying Facilities, Medicine Shops, Courier Agents, etc.

3. Food Products Sector : Finance would be available for small household packed food activities like papad , achaar making, jam / jelly making, agricultural produce preservation at rural level, sweet shops, small service food stalls and day to day catering / canteen services, cold chain vehicles, cold storage, ice making units, ice cream making units, biscuit, bread and bun making, etc.

4.Textile Products Sector : To provide support for undertaking activities such as handloom, powerloom, khadi activity, chikan work, zari and zardozi work, traditional embroidery and hand work, traditional dyeing and printing, apparel design, knitting, cotton ginning, computerized embroidery, stitching and other textile non garment products such as bags, vehicle accessories, furnishing accessories, etc.

MUDRA may be granted for other activities like :

Micro Credit Scheme : The MUDRA may be granted to financial sectors including MFIs for on lending to individuals or groups of individuals i.e. JLGs, SHGs for creation of qualifying assets as per RBI guidelines towards setting up / running micro enterprises as per MSMED Act and non-farm income generating activities.

Missing Middle Credit Scheme : Financial support to financial intermediaries for on lending to individuals for setting up / running micro enterprises as per MSMED Act and non-farm income generating activities with beneficiary loan size of 50,000 to 10 lakh per enterprise / borrower.

Refinance Scheme for RRBs / Co-operative Banks : Enhancing liquidity of RRBs / Scheduled Co-operative Banks by refinancing loan extended to micro enterprises as per MSMED Act with beneficiary loan size upto 10 lakh per enterprise / borrower for manufacturing and service sector enterprises.

Mahila Uddyami Scheme : Timely and adequate financial support to the MFIs, for on lending to women / group of women / JLGs/ SHGs for creation of qualifying assets as per RBI guidelines towards setting up / running micro enterprises as per MSMED Act and non-farm income generating activities.

Business loans for Traders and Shopkeepers : Timely and adequate financial support for on lending to individuals for running their shops / trading & business activities / service enterprises and non-farm income generating activities with beneficiary loan size of upto 10 lakh per enterprise / borrower.

Equipment Finance Scheme for Micro Units : Timely and adequate financial support for on lending to individuals for setting up micro enterprises by purchasing necessary machinery / equipment with per beneficiary loan size of upto 10 lakh.

MUDRA Recovery Process and Guarantee : The MUDRA Bank has had corpus of Rs 20,000 crore and a credit guarantee fund of Rs 3,000 crore for loan financed. MUDRA has also announced the recovery method and process for bad/NPA loan.